Roche Holding

Successfully navigating the patent cliff with a strong culture of innovation and patient care

Business

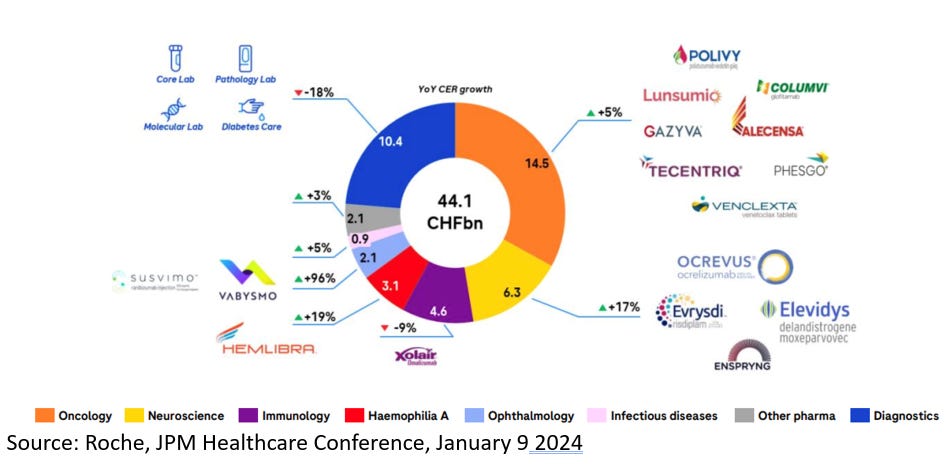

Oncology, Neuroscience, and Diagnostic equipment are the three large business areas accounting for about three quarters of total revenues. It is the area which Roche and Genentech had much success with and the one that then resulted in a stiff patent cliff. The three cancer drugs, Avastin, Herceptin, and Rituxan (AHR), had peak revenues of CHF 21B in in 2017 accounting for half of Roche’s pharmaceutical revenues. Since then, these drugs have declined by about 75% with 2023 revenues totaling at CHF 4.8B. However, Roche managed to set off all that loss of revenue with 2023 pharma revenues 3.3B higher than in 2017 while the CHF has been strong against most currencies in that period. Oncology continues to be its largest therapeutic area and that of its R&D focus as well.

Innovation

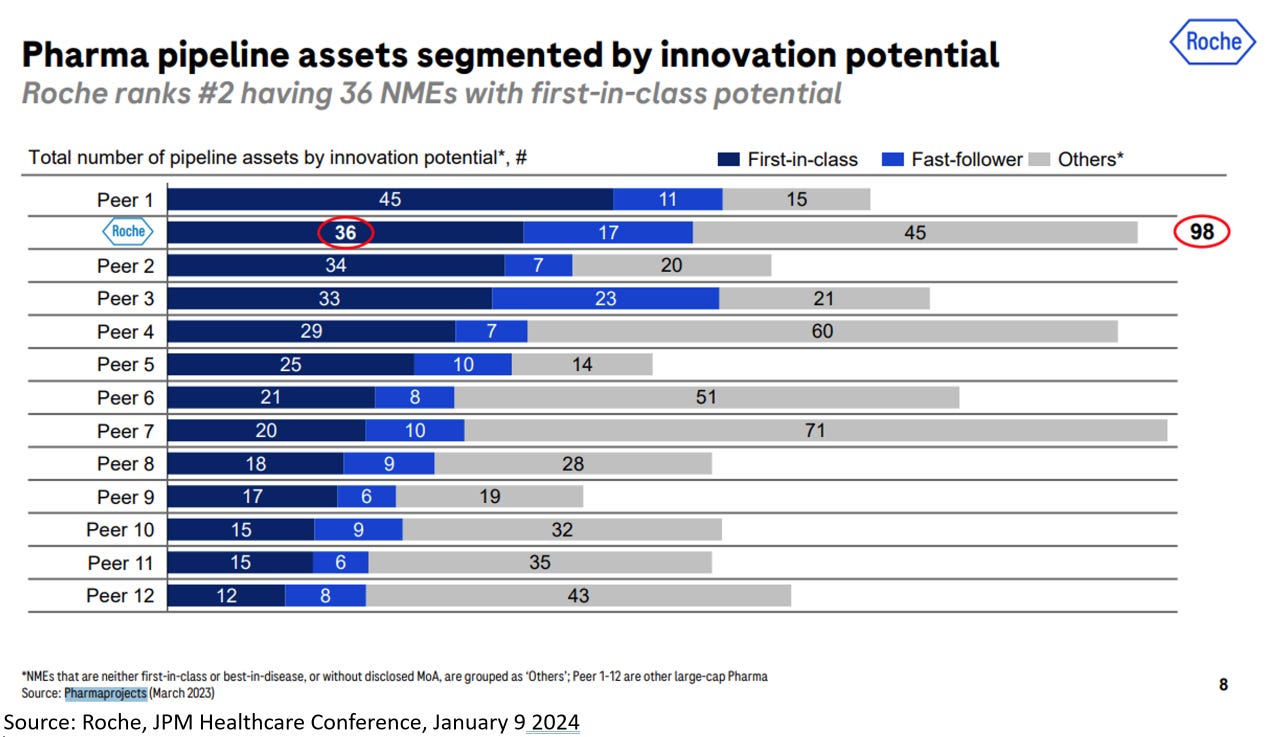

As was seen in the Large-Cap Pharma note (here), Roche scored well on innovation on most metrics. It is further seen in the chart below with the company having the second most number of novel molecules, i.e., first-in-class or best-in-disease molecules. Another indication of superior innovation is reflected in their ability to weather the patent cliff posed by the AHR drugs. Indeed, nearly half of its revenues are derived from drugs that were launched within the last 7 years.

Culture

Of course, one of the most important element for a branded pharma company is the culture of innovation. Roche score well there. However, the utmost important element is a focus on doing what is good for patients – most companies pay lip service to this element. Indeed, as we saw in the Large-Cap Pharma note, Pfizer has a poor litigation record which suggest a culture focused on commercialization as against patient benefit. On the other hand, Roche has the cleanest of the records on this count, right on par with Novo Nordisk.

Of course, this isn’t a perfect indicator – it is a backward looking indicator and if a company’s culture shifts for better or worse, it will fail to capture that.

Valuation

The stock is currently trading towards the lowest multiples of its traded history.

As against engaging into a detailed DCF by going through each molecule, making estimate with respect to each molecule, we have resorted to a much simpler valuation process. Roche has shown an ability to weather some of the largest patent cliffs with continuous and focused innovation. Accordingly, we are treating this as an enterprise that will extend its competitive advantage to periods well past the expiries of its current portfolio.

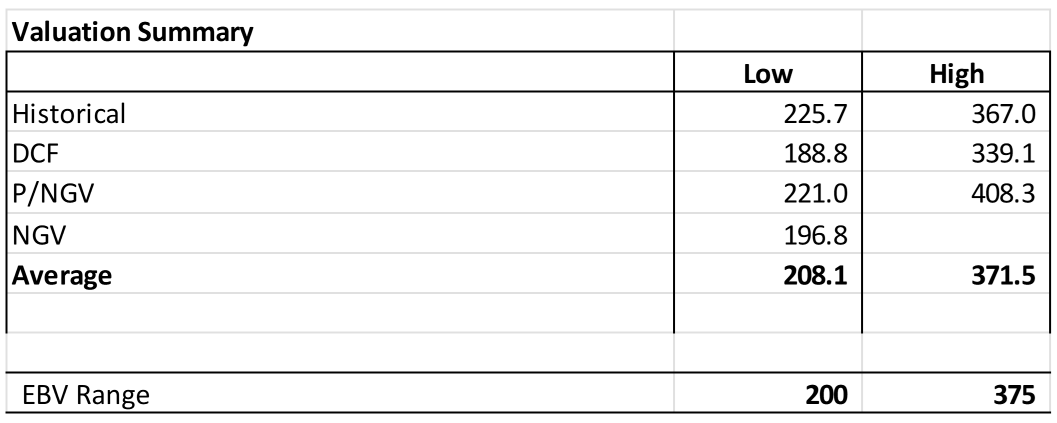

With this assumption, we have valued the company using our historical module – a stable and healthy historical performance is shown here with an almost automatic application of the historical module (using the company’s own trading multiples across conventional valuation multiples), a simplified DCF, and the P/NGV module. As seen in the table below, we assess the PB at CHF 200 – 375.

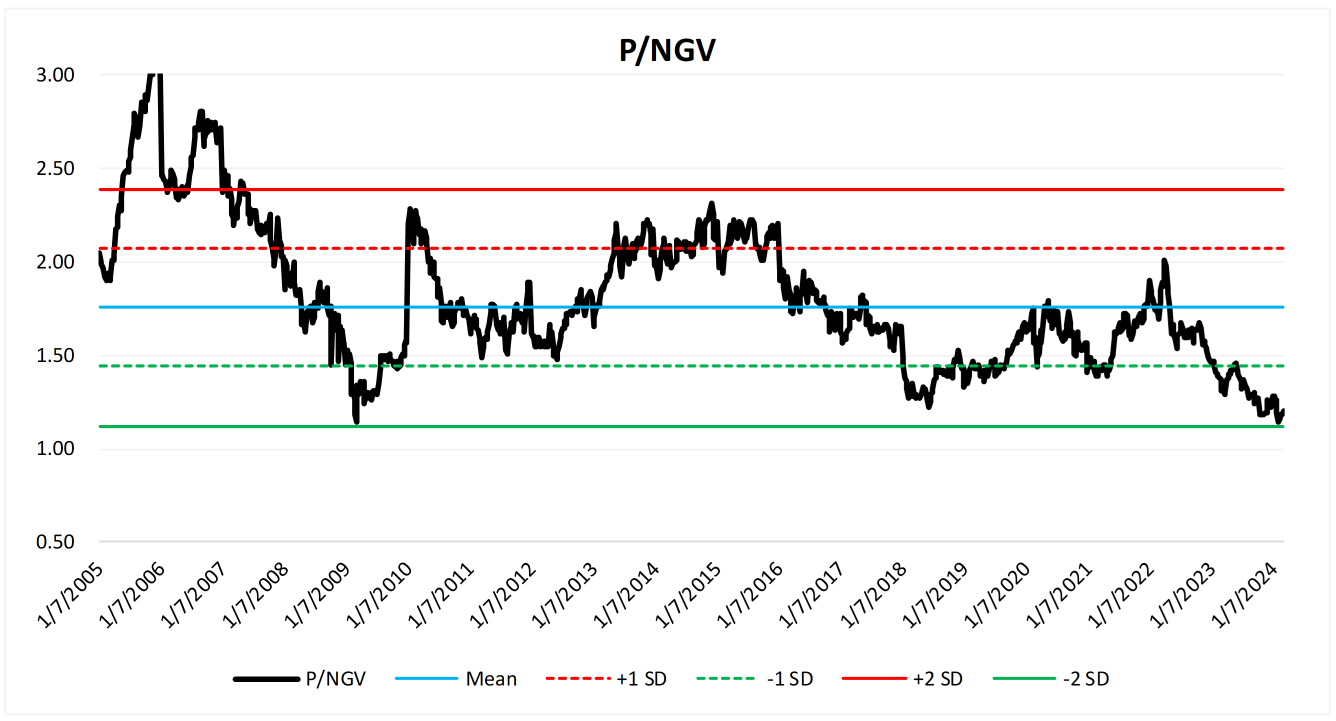

The chart below shows the stock’s trading behavior around its NGV. As is seen, it is currently trading at -2SD on P/NGV on a full period basis. At CMP, it is trading at 1.2x NGV with the NGV at CHF 200.

What do the charts say?

Chart below of the US OTC listed stock – have a longer history on this instrument. At the lower end of the channel that has been in place for nearly 3 decades. The support from 2007 highs and 2018 lows comes in about 20% lower.

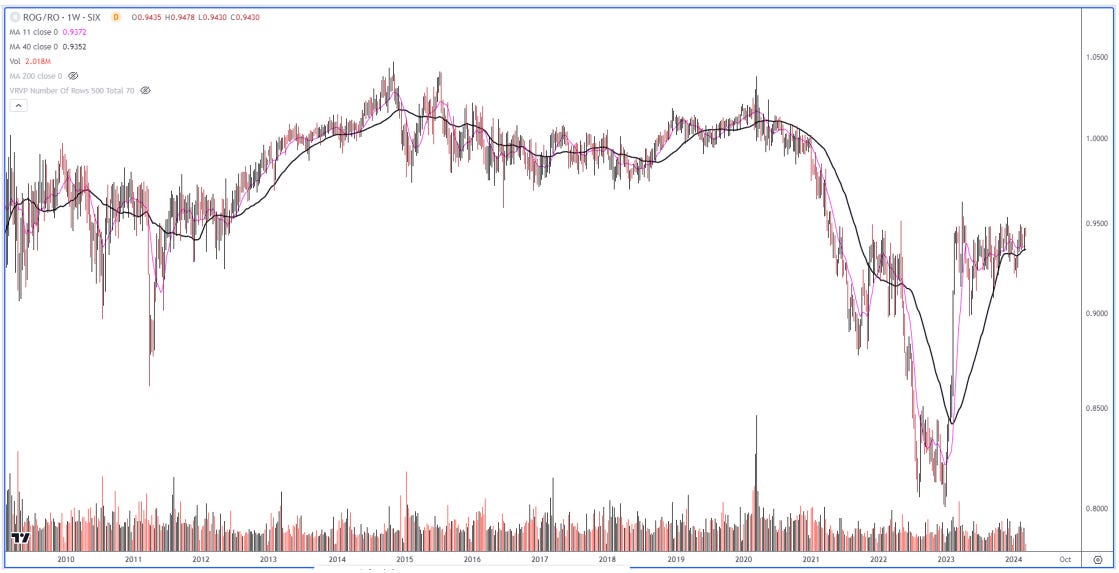

The bearer (voting) vs ordinary common shares: The non-voting shares (ROG-VX) have generally traded at a 5% discount. Between 2014 and 2020, that discount vanished. Strangely, 2022 saw an extreme widening of that discount to as much as 20%. The company repurchased 53 mln bearer shares (33% of the total) from Novartis – that buyback was likely behind the spread widening. At current prices, no meaningful mispricing exists between the two class of shares.

P.S.

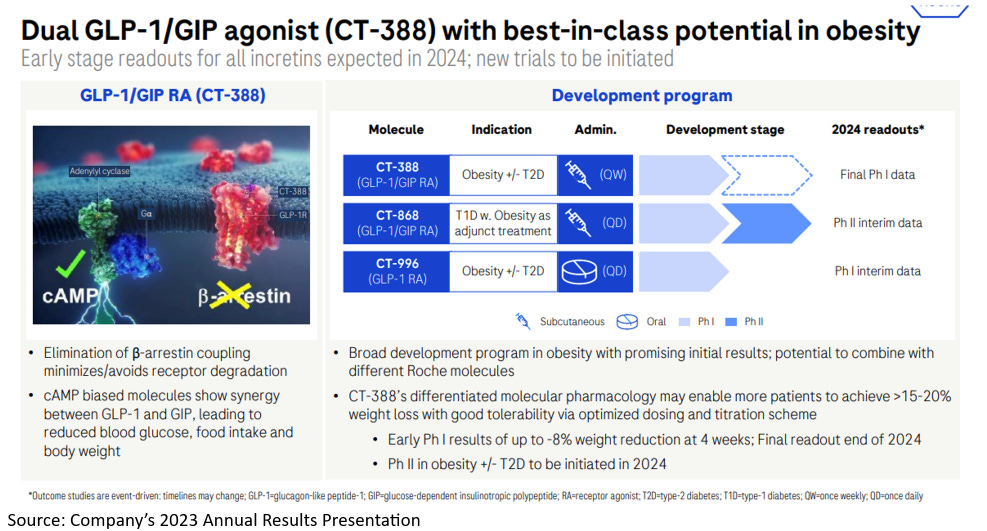

Highlighting the pipelines on GLP-1 by a large number of competitors, even Roche has a molecule in its pipeline. Early days – entering P-II this year.

I think Roche is worthy of an initiating weight within the value equities basket of the portfolio. As always, DYOD. Nothing above amounts to an investment advice.